08 October 2021

13 min read

Treasury is seeking consultation into determining the appropriateness of occupational exclusions in MySuper default insurance products, and is seeking comment on the following issues:

Treasury has provided the following potential options:

Treasury has submitted the following questions for feedback:

Submissions are due by 14 October 2021.

ASIC has identified weaknesses in some trustees’ preparedness to comply with the new internal dispute resolution requirements, including:

ASIC released Regulatory Guide ‘RG 78 Breach reporting by AFS licensees and credit licensees’, providing guidance on the new breach reporting obligations that took effect on 1 October 2021.ASIC released Regulatory Guide ‘RG 78 Breach reporting by AFS licensees and credit licensees’, providing guidance on the new breach reporting obligations that took effect on 1 October 2021.

The Government has selected its inaugural members to the Financial Regulator Assessment Authority (FRAA), appointing Nicholas Moore, Gina Cass-Gottlieb and Craig Drummond. As mentioned in our May update, FRAA will be charged with assessing both the effectiveness and capability of APRA and ASIC.

ASIC published ‘Licensing and professional registration activities: 2021 update (Report 700)’ outlining key issues, new and proposed changes to licensing processes and statistics of applications for the 2021 Financial Year. In addition to providing information on the increase of applications from the previous year (1,346 to 1,883), the report also recognises the inclusion of new licencing requirements, including authorisations to deal in superannuation and to provide a superannuation trustee service. To date, ASIC has made 57 changes to public trustees catering for the changes since 1 July 2021.

ASIC has amended and published ‘Regulatory Guide 38 The hawking prohibition’ in response to the changes to the hawking laws introduced by the Financial Sector Reform (Hayne Royal Commission Response) Act 2020.

The ATO updated its guidance for trustees requesting a deferral of member reporting obligations where it is fair and reasonable. The guidance provides useful links, including a Super Fund Reporting Deferral Request Template and references to what is considered fair and reasonable via the ATO’s Practice Statement Law Administration PS LA2011/15.

APRA wrote to all trustees outlining its intention to remove mandating independent certification of ‘priority and privilege’ insurance in APRA Prudential Standard SPS 250 Insurance in Superannuation which is set to take effect on 1 July 2022.

Priority and privilege in an insurance arrangement can be described as any arrangement whereby an insurer may be afforded an advantage such that member interests may not have been prioritised and/or where licensee trustee may be prevented from acting independently in relation to the insurance arrangements for the members of the fund. Some examples would include exclusive tender rights, excessively long contracts and limited data sharing by the incumbent insurer.

The original intention of the required independent certification of priority and privilege was to respond to the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services, which recommended priority and privilege be given to insurers to set up favourable arrangements that would be in the best financial interest of its members. However, APRA has acknowledged that such independent certification for priority and privilege may have unintended consequences due to the concepts being complex and ambiguous.

APRA determined the reporting standards developed under the first phase of its Superannuation Data Transformation project. The reporting standards are:

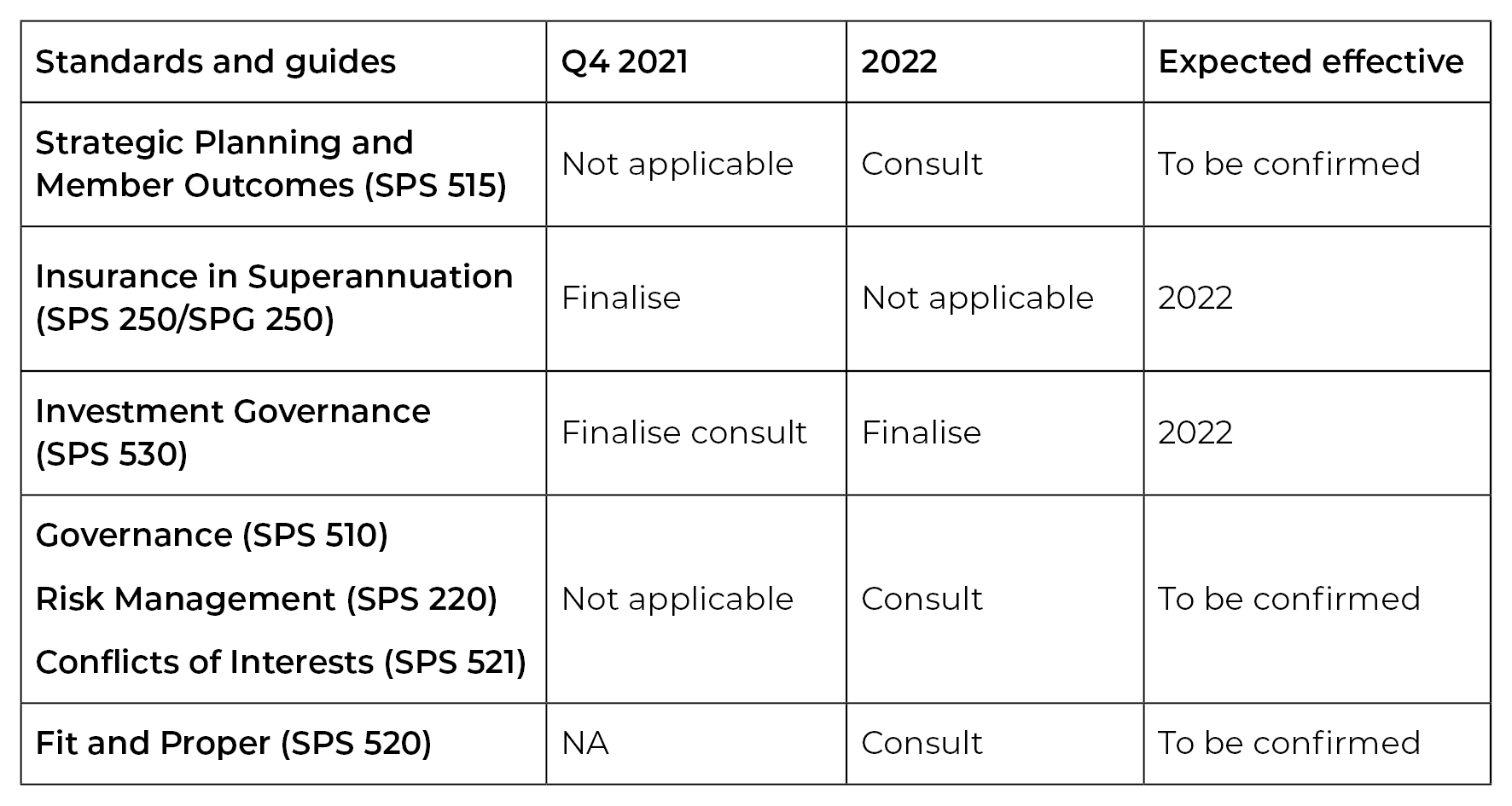

APRA updated its policy priorities for the fourth quarter of 2021, including standards for insurance in super and investment governance, ahead of a more comprehensive review of other key standards next year to ensure a sharper focus on the best financial interests duty. APRA also noted it plans to release its final guidance on managing the financial risks of climate change. The following table was also provided.

APRA released a proposed revised version of APRA Prudential Standard SPS 530 Investment Governance (SPS 530) for consultation. APRA proposes that the SPS 530 amendments will take effect from 1 January 2023.

These proposed amendments cover stress testing, valuations, and liquidity management, as follows:

1. Stress testing

The amendments propose that a trustee must complete their comprehensive stress testing program at least annually and include at a minimum:

2. Valuation

The proposed amendments include further requirements to enhance trustees’ valuation governance practices, specifically:

3. Liquidity management

The amendments propose that a trustee’s liquidity management plan must:

Submissions are due to APRA by 16 February 2022.

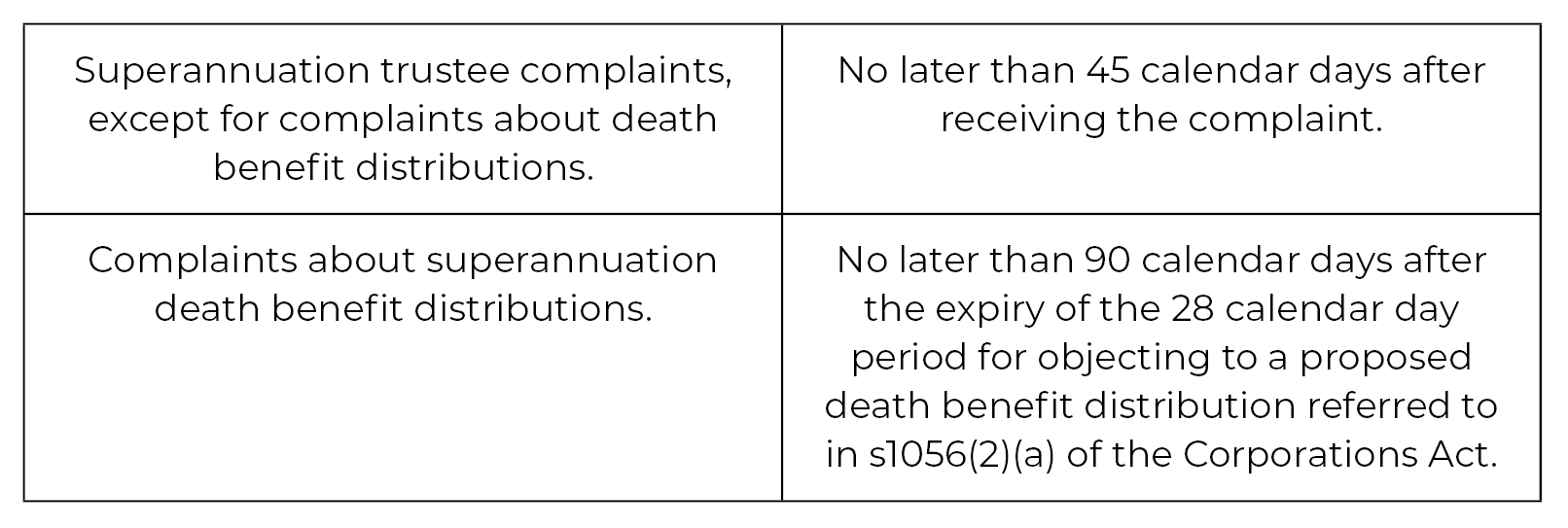

ASIC released Regulatory Guide (RG 271) Internal Dispute Resolution which, as of 5 October 2021, enforces new requirements on a trustee’s internal dispute resolutions. Unlike other ASIC Regulatory Guides, RG 271 provides enforceable requirements. We summarise trustees’ legal obligations below.

Expanded definition of ‘complaint’

Previously, expressions of dissatisfaction against staff or the organisation itself were excluded under the definition of complaint but are now included. Furthermore, social media posts on trustees’ social media channels are also defined as a complaint.

Timeframe to provide an IDR response

An ‘IDR response’ is a written communication from a financial firm to the complainant, informing them on all of the following:

The time for trustees to respond to complaints includes:

If there is no reasonable opportunity for the trustee to provide an IDR response within the timeframe, the trustee must send an ‘IDR delay notification’ that provides reasons for delay and the right to complain to AFCA.

Outsourcing the IDR process

Firms that outsource their IDR process must

Insurance in superannuation complaints

A complainant may lodge a complaint about insurance in superannuation with the insurer or the trustee. Trustees, insurers and administrators must have arrangements in place to ensure the maximum IDR timeframe is complied with regardless of the initial lodgement point. Time starts to run from the date the complaint is first lodged with either one of the parties.

Manage systemic issues

Boards must set clear accountabilities for complaints handling functions, including the management of systemic issues identified through consumer complaints. If a trustee provides reports to the board and/or executive committees, the reports must include metrics and analysis of consumer complaints, including systemic issues identified through those complaints.

Accessibility

The IDR process must be easy to understand and use, including by people with disabilities or language difficulties.

Resourcing

The IDR process must be resourced so that it operates fairly, effectively and efficiently. Therefore, the financial firm must regularly review whether the IDR process is adequately resourced.

Staff members

Staffing numbers must be sufficient to deal with complaints in a fair and effective manner within maximum IDR timeframes. This includes resourcing the IDR function to deal with intermittent spikes in complaint volumes.

Availability of complaints policy

Complaint management documentation is a key component of a financial firm’s IDR process. Firms must have a publicly available, readily accessible complaints policy and an internal complaint management procedure. Firms must provide material that explains their IDR process free of charge to complainant.

Records and reports

Financial firms must provide reports about complaints data regularly to senior management and the firm’s board (or equivalent).

Firms must record all complaints that they receive. They must have an effective system for recording information about complaints. The system must enable firms to keep track of the progress of each complaint.

The Act amends the Family Law Act 1975 (Cth) and Taxation Administration Act 1953 (Cth) to improve the visibility of superannuation assets in family law proceedings. Changes include leveraging information held by the ATO to facilitate the identification of superannuation assets.

Treasury released proposed legislation proposing new covenants that require trustees to prepare a retirement income strategy to assist beneficiaries achieve and balance the following objectives:

This includes obligations to:

Submissions are due by 15 October 2021.

The Federal Court has made declarations that Colonial First State Investments Limited (CFSIL), as trustee of the Colonial FirstChoice Fund, made false or misleading representations to members in relation to MySuper.

The Court declared that on at least 12,978 occasions, CFSIL made misleading representations regarding investment directions which may have encouraged members not to move to a MySuper product. The misleading deceptive conduct included CFSIL telling members that legislative changes required them to obtain an investment direction to stay in the FirstChoice Fund when that was not the case.

CFSIL also failed to tell members that if it did not receive an investment direction from the member, it was required to transfer the member's contributions to a MySuper product.

A penalty hearing has been listed for 12 October 2021.

On 23 August 2021, the Federal Court ordered Westpac Bank subsidiaries Westpac Securities Administration Limited (Westpac Securities) and BT Funds Management Limited (BT Funds) to pay a combined penalty of $10.5 million for failing to act in their clients' best interests.

The Court has now provided reasons for the penalty order, stating the contravening conduct was very serious and involved a deliberate and carefully planned campaign in relation to a product of particular importance to Westpac’s members. The Court noted the importance of superannuation products and “the inherent nature of superannuation as a complex investment for the long term is such that, what may seem a reasonably minor matter at the time of a decision, may have a very significant effect on a person’s financial welfare in the long term.”

APRA published additional FAQs and worked examples, providing further guidance to trustees on the reporting standards for the Phase 1 Superannuation Transformation Project.

The FAQs cover:

SRS 706.0 Fees and Cost disclosed.

Authors: Luke Hooper & Michael O’Connor

Disclaimer

The information in this publication is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavour to provide accurate and timely information, we do not guarantee that the information in this newsletter is accurate at the date it is received or that it will continue to be accurate in the future.