02 July 2026

7 min read

#Corporate & Commercial Law, #Mergers and Acquisitions

Published by:

With Australia continuing to attract significant inbound investment from Singapore and across Southeast Asia, interest in Australian M&A opportunities shows no signs of slowing. For investors looking to enter or expand in the Australian market, understanding how the deal process, structures and regulatory requirements differ from their home jurisdiction is critical to executing a successful transaction and managing risks from the outset.

This guide is a multi-part series covering the key stages of undertaking M&A in Australia, with a focus on the practical issues facing Southeast Asian investors, particularly those based in Singapore. The series follows the lifecycle of a typical transaction, from early-stage deal structuring and due diligence, including nuances of the Australian market, through to regulatory and merger control considerations, execution and post-completion integration.

In this first instalment, we outline the typical M&A process in Australia, current market trends and the key considerations before a transaction is formally underway.

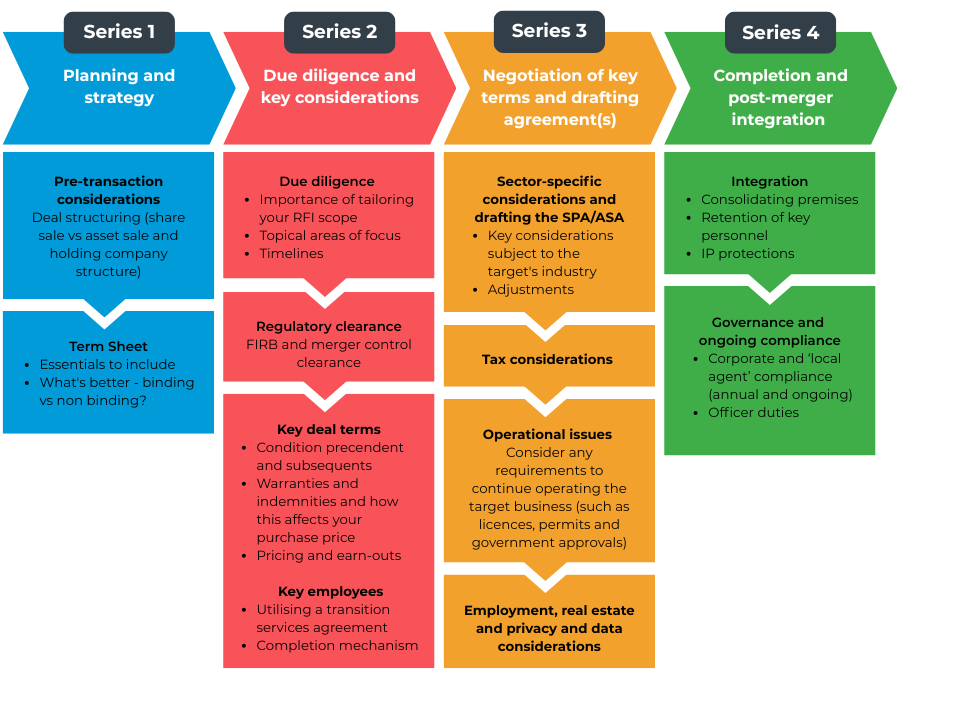

A standard M&A transaction in Australia generally progresses through four key stages: planning and strategy, due diligence, negotiation and drafting agreements, and completion and post-merger integration.

The following flowchart illustrates what is involved at each stage:

Subsequent articles in this series will explore each of these stages in more detail.

Singapore continues to be a significant source of inbound investment into Australia, reflecting its position as a key financial and commercial hub for Southeast Asia. Australia’s proximity to Singapore creates strong opportunities for mutual economic activity and investment flows. According to the Australian Bureau of Statistics, Singapore invested AU$150 billion into the Australian economy in 2025, with steady year-on-year growth and a five-year trend growth rate of 4.6%. This sustained investment comes as no surprise, given the support provided by the Singapore–Australia Free Trade Agreement, which eliminates tariffs between the two countries, among other things.

Singapore’s investments into Australia are diversified across multiple sectors, an observation noted by the Australian Department of Foreign Affairs and Trade, and is reflected in trade flows between the two markets. In 2025, Australia’s largest imports from Singapore included refined petroleum, transport services, and ships and boats, while its largest exports to Singapore were natural gas, crude petroleum and gold.

On the ground we are seeing continued investment into large-scale infrastructure and digital assets. For example, our client Lightwood Group has secured Singapore-based global asset manager Keppel Ltd as the data centre operator for a proposed AU$10 billion data centre hub on a 123-hectare site in Victoria. The project has the potential to become one of Australia’s largest sites for digital and AI infrastructure.

Additionally, we are seeing Southeast Asian corporate groups, Singaporean sovereign wealth funds and private equity firms investing in Australia’s agriculture, dairy, real estate and energy sectors. Recent significant transactions include CapitaLand Investment’s acquisition of Wingate Group in 2024 to expand its Australian private credit platform, and Singapore-listed energy company Sembcorp Industries’ proposed acquisition of Alinta Energy. These investments illustrate long-term growth strategies in Australia and the potential use of Australia as a base for broader regional expansion across Asia-Pacific.

By contrast, we have seen a shift in recent years towards opportunistic buy-side acquisitions of distressed or underperforming assets among Australian companies, typically within industries that complement their existing operations. Following acquisition, we are seeing target businesses being integrated and transitioned into the buyer’s current operations to drive efficiencies and consolidate market position.

Like in Singapore, once a target has been established, the two most common acquisition structures in Australia are:

We are finding that Singapore investors typically acquire Australian targets through an Australian acquisition vehicle owned by the Singapore parent, rather than acquiring shares directly, for asset protection and tax efficiency reasons.

Acquisitions may be executed through a structured corporate takeover, scheme of arrangement, or private treaty asset purchase. As Singaporean capital frequently involves government-linked entities or large private groups, navigating Australia's Foreign Investment Review Board (FIRB) clearance process is often a critical aspect of the acquisition process.

The nature of the target’s business, the parties involved and the buyer’s risk appetite will all inform the best structure for the transaction. A share sale structure is transactionally simpler than an asset sale and for Singaporean buyers may offer business and operational continuity as the legal entity remains unchanged. However, as the buyer acquires the target company in its entirety, a key disadvantage is that this includes all of its liabilities and any prior non-compliance, some of which may be unknown. For investors without prior knowledge of potential regulatory risks, this ought to be a key investment issue for consideration.

While the risk of undisclosed liabilities can be mitigated through robust warranty and indemnity protection and due diligence, it cannot be eliminated entirely. Share sale agreements also tend to require substantially more negotiation from the buyer’s perspective, as is the case in the Singapore market.

From a seller’s perspective, a share sale is often preferred because it offers a ‘clean cut’ exit from the business and any associated obligations and liabilities. It may also allow the seller to make use of the 50% capital gains tax discount if the shares have been held for at least 12 months. The 50% capital gains tax discount applies until 30 June 2027, after which it may be replaced with an inflation indexation model.

In contrast, an asset sale allows the buyer to select particular assets it wishes to acquire and can more easily, with the seller’s agreement, exclude any unwanted liabilities or risks. For example, a prospective buyer of a service-based target, such as a building company, may prefer an asset sale so it can carve out defect liability periods for works already completed. In contrast, in a share sale, the buyer would inherit that liability, and risk would transfer with the company. A tried and tested path in Singapore also.

However, as an asset sale only acquires specific assets, buyers should be aware of any licences which may be required to operate the target business, as not all licences can be assigned or transferred.

In both Australia and Singapore, it is common to prepare term sheets and non-binding indicative offers (NBIOs) that set out the key commercial terms of a proposed transaction.

These documents serve an important and practical purpose by ensuring the parties are aligned on the terms that matter most. In our experience, these are often price and pricing mechanics (such as a locked-box/fixed-price model or completion accounts), timing, and any material contracts or key commercial drivers. In Australia, completion accounts are more commonly used than a locked-box model, and market practice typically adopts a purchase price on a cash-free, debt-free basis with a working capital adjustment, however, we find this may differ for cross-border transactions.

In addition to the above, term sheets and NBIOs may also cover:

If any of these matters are critical to a party, or to the continued operation of the target business, they should be captured in the term sheet and/or NBIO.

While both documents are largely non-binding in nature, it is essential that certain provisions, such as confidentiality, costs, governing law and, where sought, exclusivity, are binding and enforceable. In cross-border transactions, governing law should be considered carefully to avoid potential or unintended consequences such as an inability to effectively enforce any rights.

In addition to a term sheet and/or NBIO, it is also common in Australia to have a separate confidentiality agreement that contains exclusivity provisions, particularly where the buyer and target operate as competitors or in similar industries, or where the seller wishes to ensure that target group employees are not made aware of the process.

Our next article in this series examines the due diligence process, applying for and managing regulatory approvals and key commercial terms that arise in Australian M&A transactions.

If you are considering an acquisition in Australia or have questions about the M&A process, please contact us here.

Disclaimer

The information in this article is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavour to provide accurate and timely information, we do not guarantee that the information in this article is accurate at the date it is received or that it will continue to be accurate in the future.

Published by: